Beautiful Work Info About How To Deal With Conflicts Of Interest

![Dealing With Conflicts Of Interest [12 Tips] - Jonathon Bray](https://www.jonathonbray.com/wp-content/uploads/2017/06/screenshot-2021-06-18-at-07.13.45.png)

Dealing With Conflicts Of Interest [12 Tips] - Jonathon Bray

How To Resolve A Conflict Of Interest At Workplace? | By Proofhub Blog

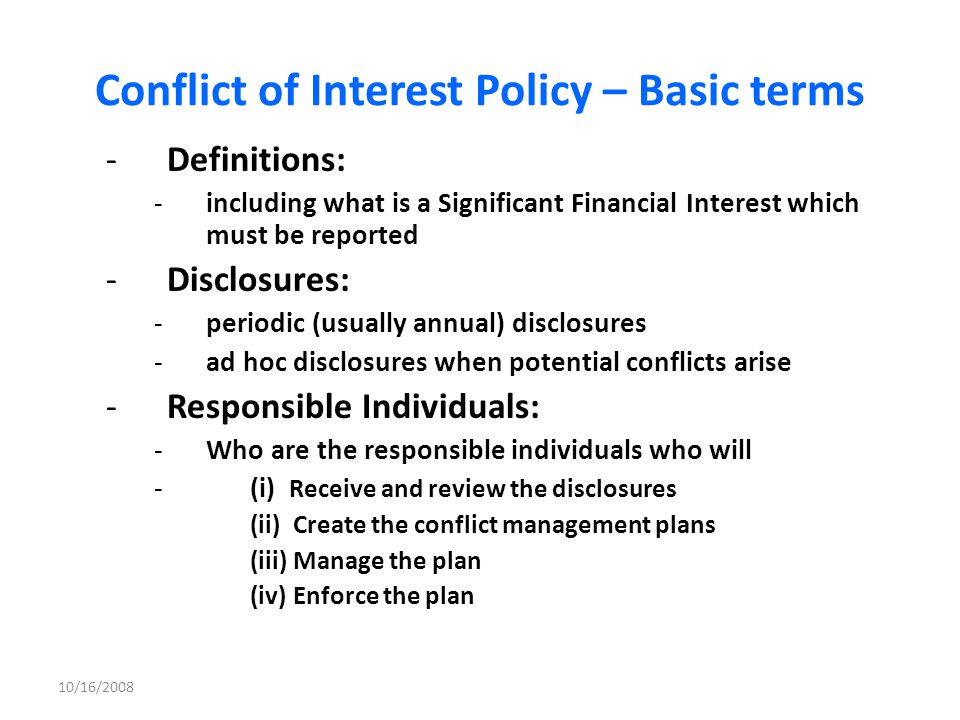

Managing Conflicts Of Interest

What You Must Know About A Conflict Of Interest In The Workplace

Conflicts Of Interest - Independent Commission Against Corruption

How To Resolve Conflicts Of Interest | The Association Corporate Treasurers

Tips for avoiding a conflict of interest.

How to deal with conflicts of interest. Define who the interested persons are. Do this early, before discussions or decisions happen. For each conflict of interest, you should consider whether the board member who has a conflict of interest should, in relation to the matter in which they have a conflict:

How to prevent conflicts of interest 1. One of the best ways to prevent conflicts of interest is by disclosing your relationships and potential conflicts with management or human resources. By anticipating conflicts of interest, and creating a system to manage them, private equity managers will be able to afford all affected constituents (and regulators).

As a group, decide the ethical standard that may work for. For example, the following restrictions in the investment advisers act of 1940 were implemented largely to avoid conflicts of interest: Steps for dealing with conflicts of interest rules to determine whether there is a conflict of interest that would prevent you from acting for a client:

How to manage a conflict of interest. Use these tips to help you avoid potential conflicts of interest in your professional life: Asking future employees directly to report any.

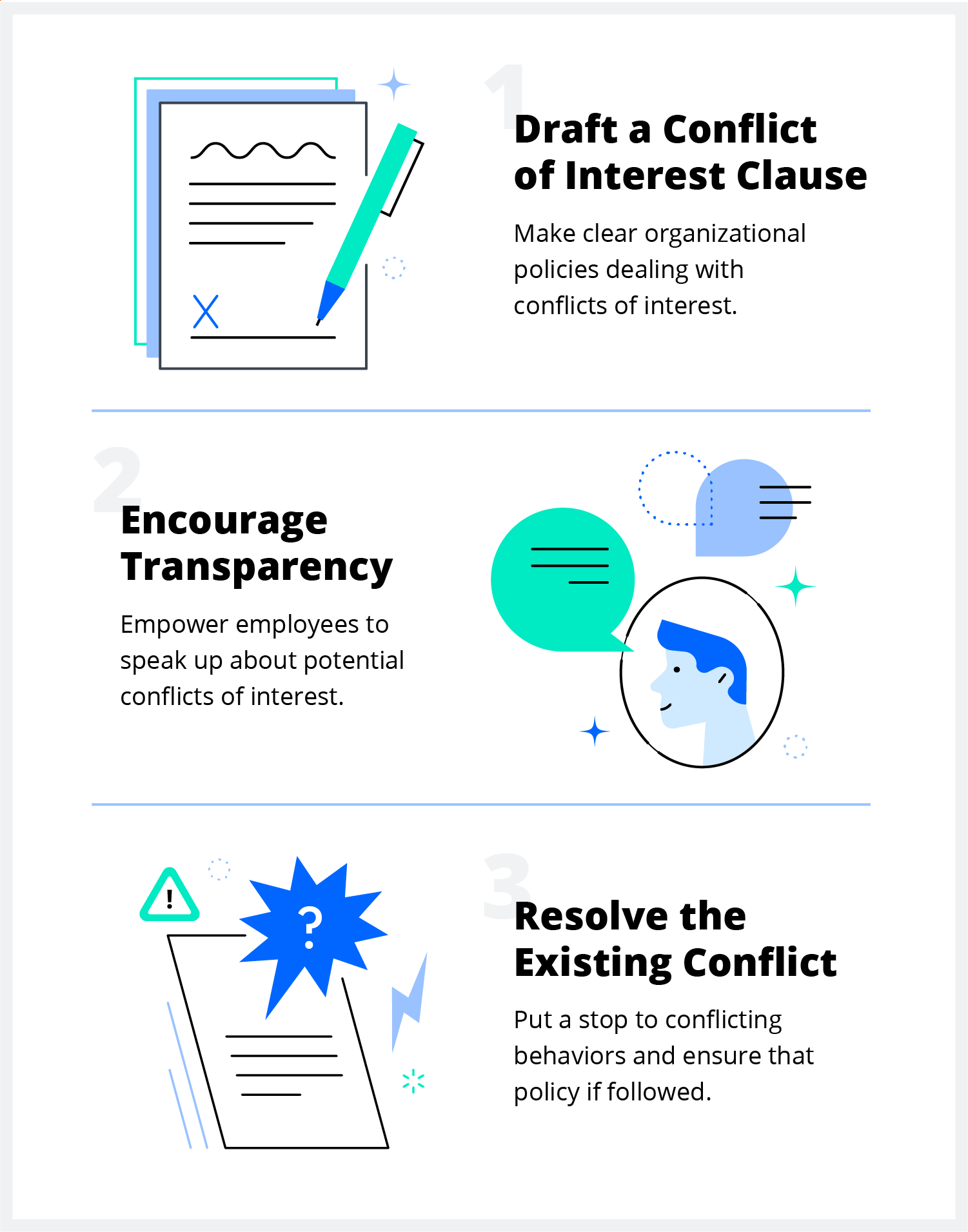

Step one of handling an employee conflict of interest is to know it’s there. Encourage employees to talk to their manager if they think they have an actual, perceived, or potential coi. By laying out clear policies, collecting all the information you need from employees, and having signed documents, you can help prevent conflict of interest situations.

Perception happens when an individual. Use the caucus as a forum to air possible situations where members may have conflicts. Tial conflicts of interest before they arise.

Craft a simple, yet clear policy and explain as. Detail which types of relationships potentially represent conflicts of interest and thus need to be. It all starts with the right policy.

Declare conflicts of interest (step 1) you must tell the other trustees if you personally have a conflict of interest. Try to acknowledge each other on the points on which you both agree. Transparency (being completely open and frank) becomes important when dealing with both actual and potentially perceived conflicts of interest.

(i) the qualified client rule where the. First, determine if there is a conflict of.

/CONFLICT-OF-INTEREST-FINAL-SR-03da98f0411e4bec9da01a5f09a71b8b.jpg)

Conflict Of Interest Definition

Conflicts Of Interest In A Nonprofit

Managing Conflict Of Interest | Download Scientific Diagram

Conflict Of Interest | Compliance Services

20 Examples Of Conflicts Interest At Work - Everfi

Conflicts Of Interest | The Pensions Regulator

Steps For Managing Conflicts Of Interest. | Download Scientific Diagram

Conflict Of Interest: The Complete Small Business Guide | Legalzoom

Managing Conflicts Of Interest Guide | Acnc

How To Manage Conflicts Of Interest In Your Organization

Managing Conflicts Of Interest - Ppt Download

Handling Conflicts Of Interest: 7 Simple Steps To Follow

Conflict Of Interest At Work And Its Compliance Implications | Vinciworks